Australian industrial property has been one of the most consistent performers in commercial real estate over the past decade, and the latest data confirms that story is far from over. The December 2025 MSCI results show industrial delivering total returns of 8.6 per cent, underpinned by capital growth of 4.1 per cent, the strongest capital appreciation of any major asset class. Against a national backdrop of 2.0 per cent capital growth across all property marking a genuine turning point after two years of market correction, industrial continues to set the pace.

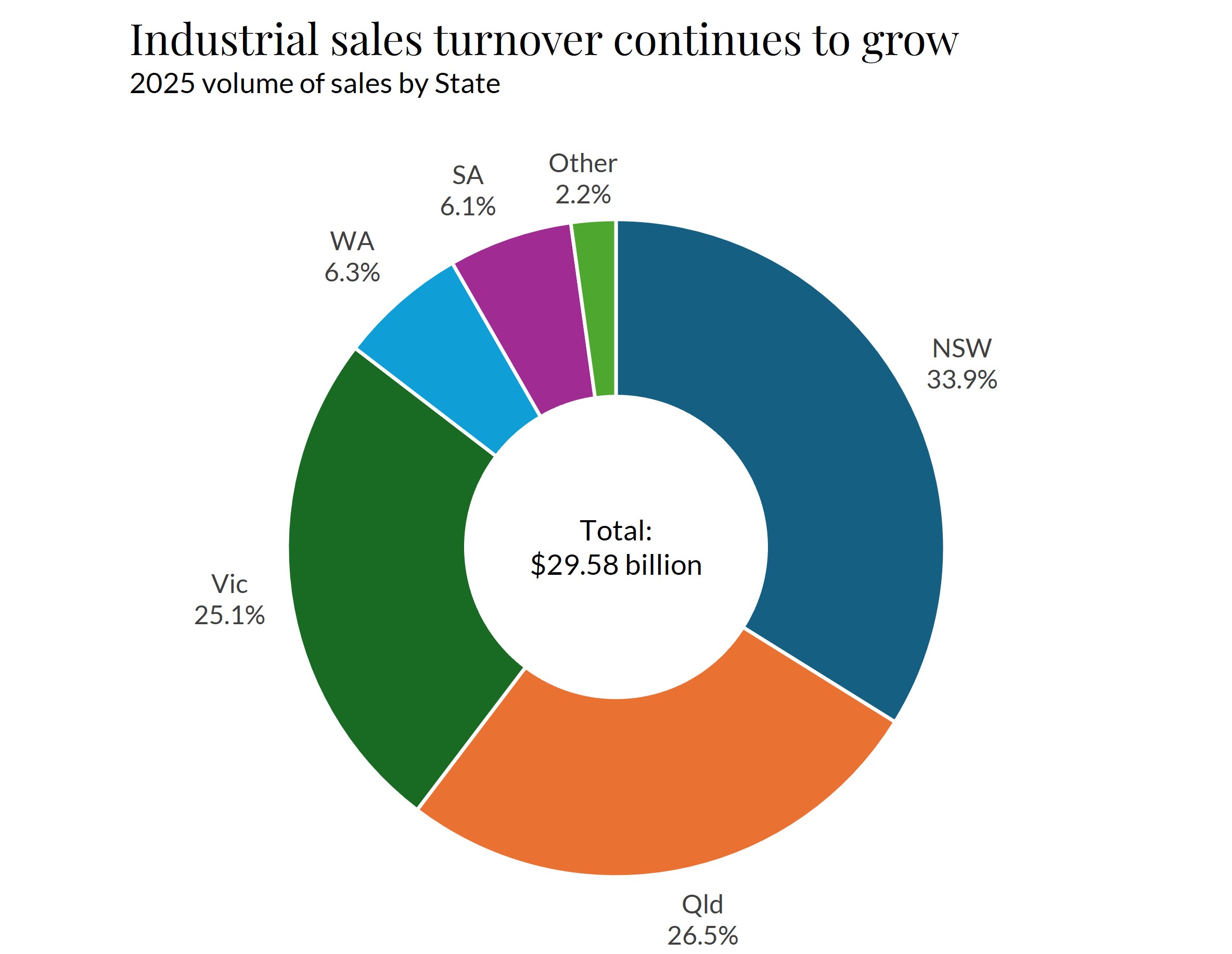

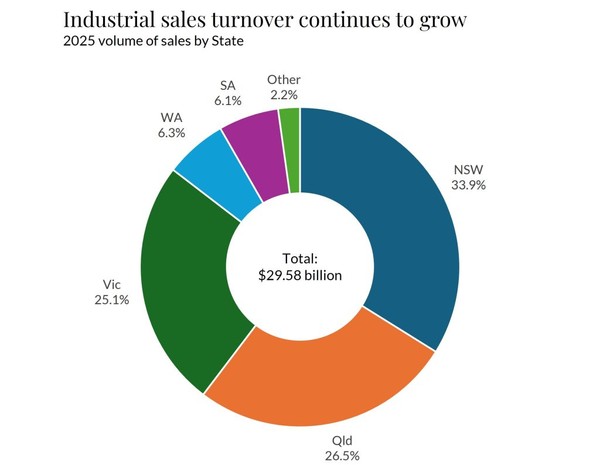

Transaction volumes reinforce this. Industrial was Australia’s most-traded asset class in 2025, with $29.58 billion changing hands across the year, up 44.9 per cent from 2024, accounting for 36.8 per cent of all national commercial property activity. Average transaction sizes have grown too, reaching $6.01 million as buyers increasingly recognise that existing stock carries genuine scarcity value. Queensland led in momentum, with Brisbane nearly doubling its volumes to $7.84 billion, while Sydney remained the dominant market. The depth and consistency of this activity, drawing institutional capital from Canada, Singapore and the United States alongside domestic super funds and REITs, reflects a market that global investors continue to regard as fundamentally undersupplied.

But beneath the headline performance figures, a more structural shift is underway, one that will reshape not just how industrial property is operated, but how it is valued and what it needs to deliver.

Artificial intelligence is rapidly moving from a back-office tool to the engine room of modern warehouse and logistics operations. Automated storage and retrieval systems, autonomous mobile robots and AI-powered inventory management are becoming standard fitout in the most sought-after facilities globally. This is well advanced in the United States with the warehouse automation market projected to more than double from US$25 billion in 2024 to over US$54 billion by 2029, with Amazon providing the clearest indication of where the trajectory leads, targeting 30 to 40 per cent automated order fulfilment by 2030.

Australia is not immune to these pressures, and in many respects the local market is well positioned to benefit. The country’s persistent labour cost challenges and the concentration of e-commerce and logistics activity along major metropolitan fringe corridors create the same economic incentives for automation that are driving investment in facilities overseas. The transport, postal and warehousing sector recorded 5.1 per cent business growth in the year to June 2025 according to the ABS, among the fastest growing industries in the country, adding further demand pressure to industrial markets already operating with constrained vacancy. The question for Australian landlords and developers is no longer whether occupiers will demand AI-ready buildings, it is how quickly that demand will materialise and which assets will be left behind. The NSW Government’s Employment Lands Development Monitor, released in December 2025, makes the supply challenge concrete. Of the 20,210 hectares of zoned employment land across Greater Sydney, just 631 hectares of undeveloped land has access to water and sewer connections, representing less than 9 per cent of all undeveloped stock. Almost all of it sits in Western Sydney, concentrated around the Aerotropolis precinct in Penrith, Blacktown, Fairfield and Liverpool. The data is a stark reminder that for the vast majority of established Sydney industrial markets, developable land is effectively exhausted. As the logistics industry moves toward AI-driven automation that demands larger, more technically specified facilities, the land capable of accommodating those buildings is further from the city than ever. Getting more out of existing, well-located stock through smarter design and technology is not just an opportunity, it is becoming a necessity.

The implications for building specification are significant. AI-enabled automation systems require substantially greater power capacity than conventional warehousing, along with high-bandwidth data infrastructure, enhanced temperature control for robotic systems and redundant power supply to protect substantial capital investment in automation equipment. Assets that can meet these requirements will command premium rents and attract the strongest tenants. Those that cannot face growing obsolescence pressure, a prime versus secondary divide that is already playing out in leasing markets across Sydney and Melbourne.

The relationship between AI and overall demand for industrial space is genuinely complex. On one hand, smarter and more responsive supply chains drive e-commerce growth, creating additional need for distribution capacity. On the other, more efficient inventory management and denser automated storage configurations can reduce the total footprint required to service the same volume of goods. Some operators are already reporting meaningful reductions in space requirements as automation matures. The net effect on aggregate demand is uncertain, but what is more predictable is a shift in the composition of that demand, toward well-specified, technology-capable assets in locations with strong logistics connectivity, and away from ageing secondary stock that cannot meet the operational requirements of the next generation of occupier.

For investors, the near-term picture for industrial property remains among the most attractive in the commercial sector. Supply constraints, population growth and the continued structural shift toward online retail provide a solid floor. But the medium-term opportunity lies in understanding which assets are positioned to meet tomorrow’s occupier requirements, and capitalising on a market where the gap between the best and the rest is only going to widen.

________________________________________________________________

Vanessa Rader | Head of Research | Ray White Corporate